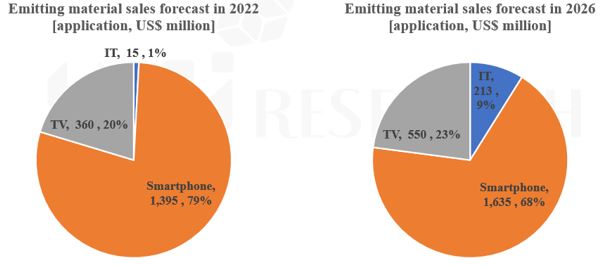

Fierce Price Competition Amongst WOLED TVs, QD-OLED TVs, and Neo QLED TVs

We experienced fierce price competition in the first half of 2022 among premium TVs with a launch price of $2,000 or more. It will be interesting to see how the Amazon Prime Day event scheduled for July will affect TV prices.

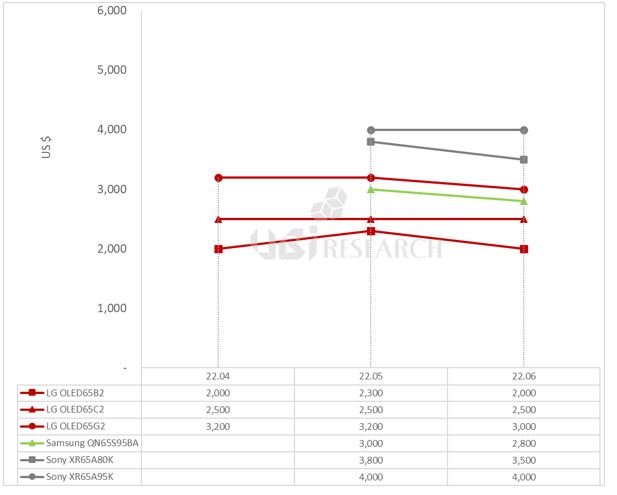

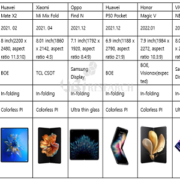

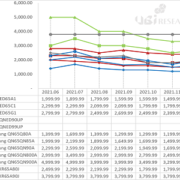

2022 OLED TV prices until June 2022 was analyzed based on 65 inch TVs. The standard was the selling price on Bestbuy.com and Sony’s QD-OLED TV selling price on their official website.

LG Electronics’ WOLED TVs B2, C2, and G2 released in March were $2,300, $2,500, and $3,200, respectively. Samsung Electronics’ QD-OLED TV S95B was $3,000. Sony’s WOLED TV A80K was priced at $3,800 and QD-OLED TV A95K was priced at $4,000.

In June, the price of LG Electronics’ G2 model fell by $200, forming a price difference of $500 for each series. Samsung Electronics’ S95B model continues to maintain a price difference of $200 lower than LG Electronics’ high-end model G2. Sony lowered the price of the WOLED TV A80K by $300, while maintaining the price of QD-OLED TV A95K.

Samsung Electronics’ S95B and LG Electronics’ high-end OLED TV G2 are in heavy price competition. Sony is setting the price of QD-OLED TV higher than WOLED TV.

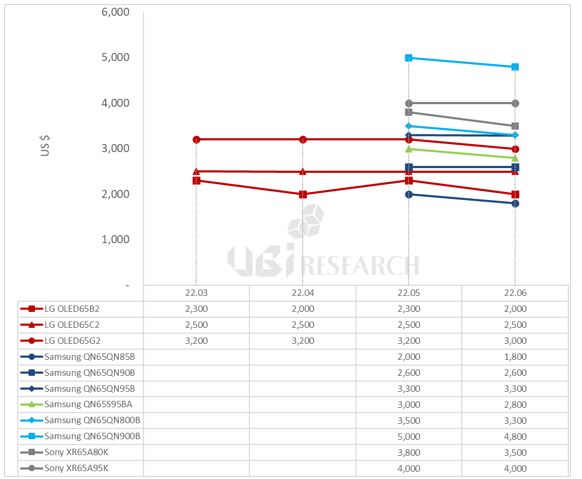

The price competition is also fierce between OLED TVs from each set makers and Neo QLED TVs with Samsung Electronics’ mini-LED technology.

As of June, the prices of Samsung Electronics’ 4K Neo QLED TVs, QN85B, QN90B, and QN95B, are $1,800, $2,600, and $3,300, respectively. The 8K Neo QLED TVs QN800B and QN900B are $3,300 and $4,800.

The prices of Samsung Electronics’ 4K Neo QLED TV series and LG Electronics’ 4K OLED TV series are similar. Within Samsung Electronics’ entire TV series, QD-OLED TV is located between 4K Neo QLED and 8K Neo QLED. Sony’s OLED TV series, which is highly evaluated in terms of picture quality, is competing in price with Samsung Electronics’ 8K Neo QLED TV series.

Although this price trend is expected to continue this year, aggressive marketing following the Amazon Prime event in the second half of the year and the Qatar World Cup is expected to be strong variables. Attention should be paid to how LG Electronics’ OLED TV with micro lens array technology, which is expected to be released next year, will affect the premium TV market in the future.

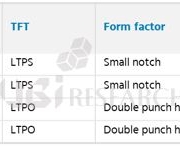

Galaxy Note 20 Ultra with LTPO applied

Galaxy Note 20 Ultra with LTPO applied

http://olednet.com/wp-content/uploads/2021/03/oled4.jpg

http://olednet.com/wp-content/uploads/2021/03/oled4.jpg