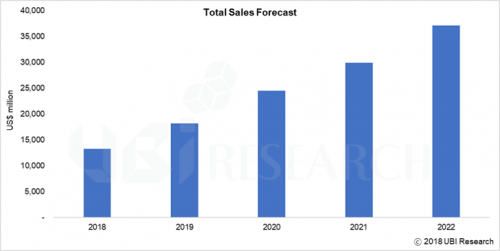

Market for OLED materials and components is forecast to grow to US$37 billion in 2022.

In the 2018 OLED material and component report and Market Track published by UBI Research, the entire market for OLED materials and components market is expected to grow at a CAGR of 29% by 2022, forming a market of US$ 37 billion in 2022.

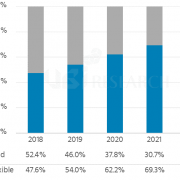

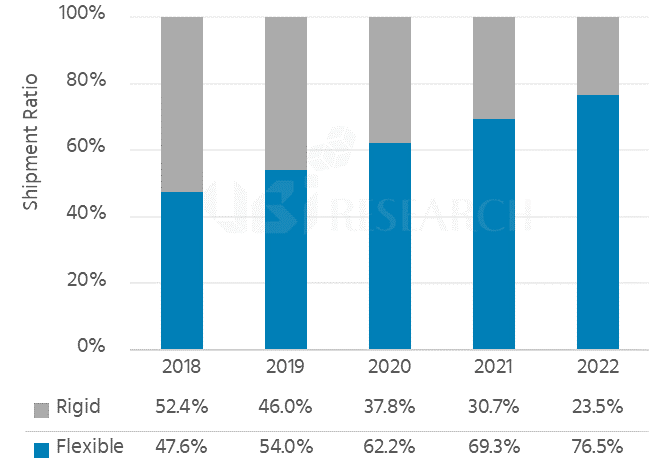

<Market forecast for OLED materials and components>

The overall OLED material and component market forecasted in this report is calculated based on the panel makers’ available capacity and includes all the materials and components for OLED production.

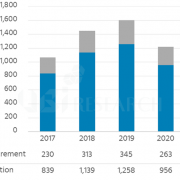

The total OLED material and component market is counted as US$ 9,794 million in 2017 and is expected to grow by 35% to US$ 13,264 million in 2018.

Major growth drivers are mentioned as capacity expansion of Samsung Display and LG Display inclusive of Gen6 flexible OLED mass production lines of Chinese panel makers.

UBI Research commented “Utilization of Samsung Display in the first quarter of 2018 was poor, but it is turning to normal from the second quarter, and LG Display and Chinese panel makers are also aiming to mass-produce this year. In particular, it will have a major impact on the growth of the materials and components market in 2018 whether Samsung Display’s A4, LG Display’s E5, E6 and BOE’s B7 lines will be in full operation.”

In the 2018 OLED material and component report, the market is forecast for 20 kinds of major materials and components used in OLED for mobile devices and large-area OLED, including substrate glass, carrier glass, PI and organic materials for TFT. In addition, the report covers industry trends and key issues related to the core materials, while Market Track forecasts the expected purchase volume and purchase amount by panel makers.